|

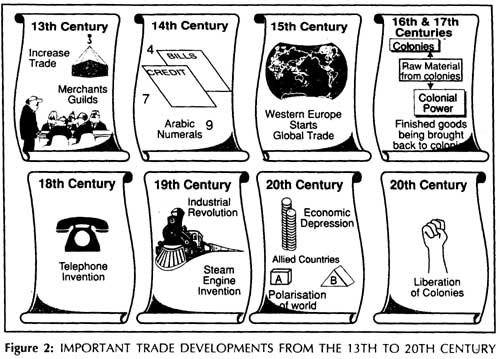

Origins and Development of Trade in the Early Stages Global trade existed in the form of barter in the Egyptian, Mesopotamian, Indus Valley, Phoenician and Chinese civilizations as far back as 4000 BC to 1000 BC. Trade also took place between Africa and Egypt and the Tigris Valley, with Africa exporting wood and ivory, and importing utensils and precious metals. Initially trade comprised products which were coveted in different countries: pelts and tobacco coming in from the West to the East and spice, jewellery, gold, silver and pottery going from the East to the West. The earliest monetary units were introduced in 700 BC by Lidia, a country in the Aegean region of Europe (now part of Turkey), followed by Persia. The design and size of the coin determined the value of each piece of currency. Trade boomed between Europe and Asia with the conquests of Alexander the Great in 400 BC, taking place mainly between Greece and Rome in the west, and between the Middle East and India. Around this time the large-scale production of goods mainly for export began as did professional, specialized trading. The Greeks and Romans brought ships to ports in the east and sold their goods to buyers directly from the ships. Improvement in ship design, the development of the compass and the use of astronomy for guiding vessels accelerated trade as -most trade took place via ships. Similarly, the development of the rudder helped improve control over ships and made travel to distant places easier. Between the years 200 AD and 600 AD, during the reign of the Hun Dynasty in China, overland trade routes were opened to India and the Mediterranean. Later, around 700 AD, China commenced trade with Japan and Korea.

After the decline of the Roman empire, Byzantium in Turkey (which was later Constantinople and is today Istanbul) was the trading capital between the east and the west. It was the largest city in the world at that time and its currency was widely accepted. This widespread recognition of currency was a landmark in the development of global commercial activity. There was a general decline in trade from the 5th to the 12th century following the fall of the Roman empire and the advent of the church. The church did not encourage mercantilism and enforced trade controls. Shifts in Trade Patterns The need for the production of goods for export to keep the economies of western Europe active led to the formation of merchants guilds in Europe in the 13th century. From the end of the 15th and early -16th centuries certain very rapid economic, social, and cultural changes occurred in western Europe. States began to regulate global trade which was stimulated by the Protestant reformation's attitude of tolerance towards the accumulation of wealth. Important influences on trade at this time were the formation of the national states as political entities, and monopoly controls over business by rulers in the granting of specific and exclusive rights to trade. Colonisation by Spain, Portugal, Great Britain and France in the 16th and the 17th centuries led to a rapid expansion of global trade with raw materials being shipped from colonies and finished goods being shipped back. All these developments resulted in a need for expansion of capital and laid the foundation of the modem corporation. Chartered rights were granted for exclusive trade in exchange for certain obligations to the state. Subsequently the joint stock company also came into being and ensured that the life of a company was not to be linked exclusively to one individual. One of the earliest companies to be granted exclusive trading rights was the Hudson Bay Company which in 1670 had rights for exclusive trade in northern America where it formed a chain of retail outlets. Similarly, the East India Company was granted exclusive trade rights in India at the end of the 17th century. Between the 18th and 19th centuries, with the advent of the industrial revolution, several companies began to market their products in the world market in an organized and effective manner. This was the beginning of the modern global corporation which used techniques such as marketing. Among the first transnational companies to develop during the 19th century were Unlived of Holland and England, Imperial Chemical Industries of England, Anglo Swiss Condensed Milk Company of Switzerland, Philips Lamps of the Netherlands and Standard Oil of the USA. Unilever started operations around 1882 - 1890 and became internationally known around 1929. American firms were innovative, created new products and marketed aggressively. Cable development in the late 18th century and the transcontinental railways provided further impetus to American business. Singer's was one of the first American companies successful in Europe and then branching out to other parts of the world. Factors giving Impetus to Global Business in the 20th Century The 20th century has seen rapid development in global business largely influenced by the following factors: Polarisation of the World. The polarisation of the world into warring groups during the two world wars resulted in intensive Cooperation for success in the war among allied nations on both sides. Besides cooperation in weapons production and war strategies, there was the need to share all required resources such as food, cloth, oil and other fuels. Political Blocs. Prior to World War II the USA and the USSR were trade partners and the USA was a large exporter to the Soviet Union. In the post-World War II period, the advent of the Cold War resulted in a drop in trade. Exports to the Soviet Union from the USA depended upon substantial year-to-year changes on account of political relationships and agreements. This caused changes in the pattern of trade and an increase in exports to the USSR from countries like Austria, Finland, France and West Germany. Economic Depression. The economic depression in the western world in the 1930s led to a need for mutual readjustment among western nations to promote economic revival. This process was accelerated by post-war needs for economic stability and growth. Revolution in Communication. The revolution in communications technology, advancements in industrial mass production techniques, and more recently in electronics, resulted in a very rapid expansion of global business. Polarisation of Political Systems. The polarisation of developed countries into developed capitalist and communist countries also resulted in a growing global exchange of goods and services among these groups, as well as between them and developing countries. Liberation of Colonies. Liberation of colonies in Asia, Africa and Latin America and their subsequent quest to raise standards of living resulted in an impetus to global business activity. Reconstruction of Defeated Nations. The reconstruction of defeated nations, notably Japan and West Germany, gave impetus to technological development and economic activity.

|